Imagine you’ve just started a small business a grocery shop in your neighborhood. At the end of the day, you sit down with your notebook to record everything: money coming in from customers, payments made to suppliers, and daily expenses like electricity and rent. At first, it may seem simple, but as transactions grow, confusion begins. Where should you record incoming cash? What about money you owe? This is exactly where understanding the difference between debits and credits becomes essential.

In accounting, every financial activity is recorded using a structured system, and the core of that system lies in understanding debits vs credits. These two terms may sound technical, but they are actually simple once you grasp their purpose. The difference between debits and credits helps you track how money flows in and out of a business. Whether you’re managing personal finances, running a company, or studying accounting, knowing debits vs credits ensures your records remain accurate and balanced.

Think of it like a balance scale every transaction has two sides. This balance is what keeps financial systems reliable across the world. Without understanding both, even a small mistake can lead to major confusion in financial reports. That’s why mastering the difference between debits and credits is not just important it’s absolutely necessary for financial clarity and success.

Debits vs Credits Key Difference

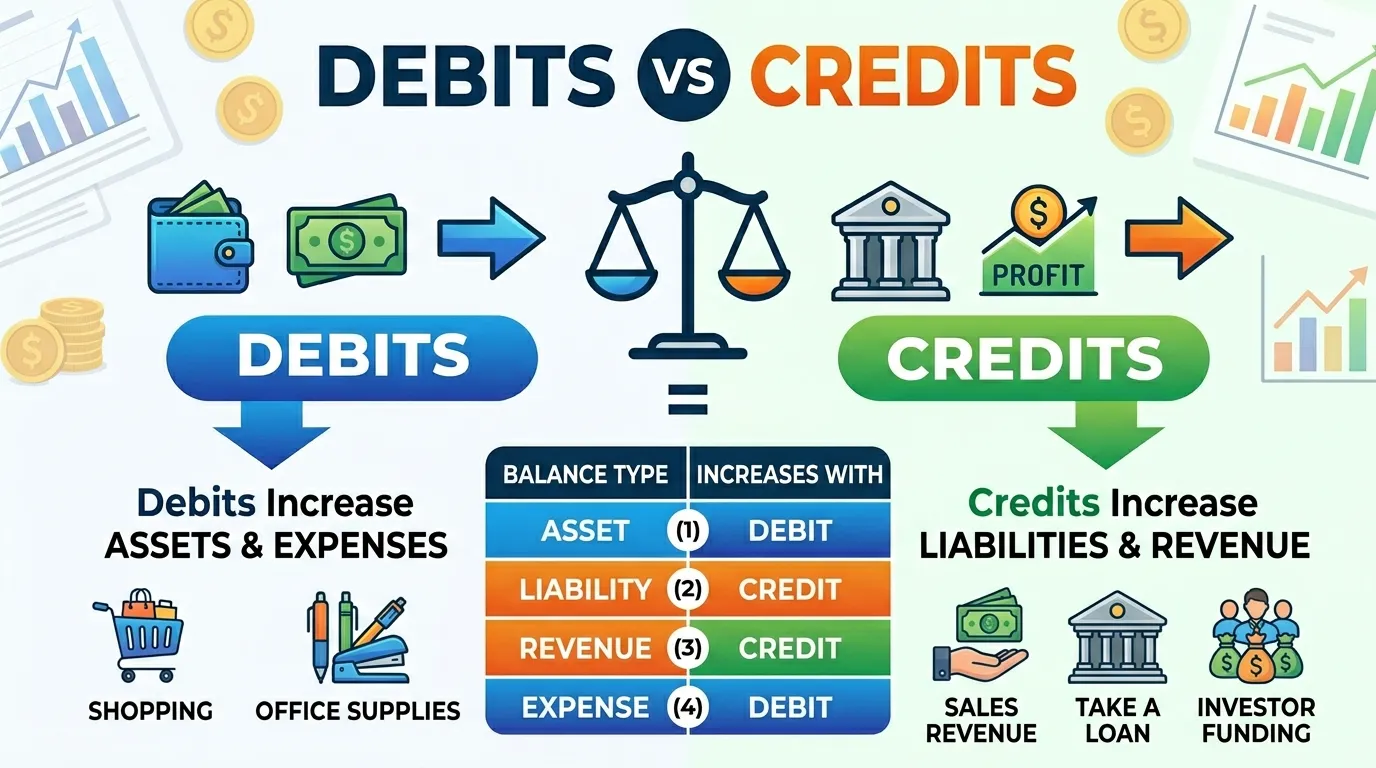

The primary difference between debits and credits lies in how they affect accounts:

- Debits increase assets and expenses but decrease liabilities and equity.

- Credits increase liabilities and equity but decrease assets and expenses.

In simple terms, debits represent incoming value, while credits represent outgoing value—depending on the type of account.

Why Is Their Difference Necessary to Know?

Understanding the difference between debits and credits is crucial for both learners and professionals. It forms the foundation of accounting systems used worldwide. Without this knowledge, financial records would become inconsistent and unreliable.

For students, it builds a strong base in accounting and finance. For professionals, it ensures accuracy in bookkeeping, auditing, and reporting. In society, businesses rely on proper accounting to maintain transparency, pay taxes correctly, and build trust with stakeholders. Even individuals benefit from understanding these concepts for personal finance management.

Pronunciation of the Both (US & UK)

- Debits

- US: /ˈdɛbɪts/

- UK: /ˈdebɪts/

- Credits

- US: /ˈkrɛdɪts/

- UK: /ˈkredɪts/

These pronunciations lead us into the deeper understanding of how these terms function in real accounting systems.

What is the Difference Between Debits and Credits?

1. Definition

- Debits: Entries recorded on the left side of an account.

- Example 1: Cash received from a customer is recorded as a debit.

- Example 2: Purchasing furniture increases assets, so it is debited.

- Credits: Entries recorded on the right side of an account.

- Example 1: Revenue earned is recorded as a credit.

- Example 2: Loan taken increases liability, so it is credited.

2. Position in Ledger

- Debits: Always on the left side.

- Example 1: Debit side shows expenses like rent.

- Example 2: Debit records inventory purchases.

- Credits: Always on the right side.

- Example 1: Credit side shows income.

- Example 2: Credit records capital investment.

3. Impact on Assets

- Debits: Increase assets.

- Example 1: Cash received increases asset.

- Example 2: Buying equipment increases assets.

- Credits: Decrease assets.

- Example 1: Paying cash reduces asset.

- Example 2: Selling equipment reduces asset value.

4. Impact on Liabilities

- Debits: Decrease liabilities.

- Example 1: Paying off a loan reduces liability.

- Example 2: Settling accounts payable decreases liability.

- Credits: Increase liabilities.

- Example 1: Taking a loan increases liability.

- Example 2: Buying on credit increases payable.

5. Effect on Equity

- Debits: Decrease equity.

- Example 1: Owner withdrawal reduces equity.

- Example 2: Losses decrease capital.

- Credits: Increase equity.

- Example 1: Owner investment increases equity.

- Example 2: Profit increases capital.

6. Role in Expenses

- Debits: Increase expenses.

- Example 1: Paying rent is a debit.

- Example 2: Utility bills recorded as debit.

- Credits: Decrease expenses.

- Example 1: Refund on expenses reduces cost.

- Example 2: Discount received lowers expense.

7. Role in Revenue

- Debits: Decrease revenue.

- Example 1: Sales return reduces revenue.

- Example 2: Allowances decrease income.

- Credits: Increase revenue.

- Example 1: Sales income recorded as credit.

- Example 2: Service income credited.

8. Use in Double-Entry System

- Debits: One side of every transaction.

- Example 1: Debit cash, credit sales.

- Example 2: Debit expense, credit cash.

- Credits: Opposite side of transaction.

- Example 1: Credit revenue when cash received.

- Example 2: Credit liability when loan taken.

9. Balance Nature

- Debits: Typical balance for assets and expenses.

- Example 1: Cash account usually debit.

- Example 2: Expense accounts show debit balance.

- Credits: Typical balance for liabilities and income.

- Example 1: Loan account has credit balance.

- Example 2: Revenue accounts are credit.

10. Visual Representation

- Debits: Represented on left side in T-account.

- Example 1: Left column entries are debits.

- Example 2: Debit side increases asset value.

- Credits: Represented on right side.

- Example 1: Right column entries are credits.

- Example 2: Credit side shows income growth.

Nature and Behaviour of Both

Debits and credits behave differently depending on the type of account. Debits naturally increase assets and expenses, making them essential for tracking resources and costs. Credits, on the other hand, increase liabilities, equity, and revenue, reflecting obligations and income. Their interaction ensures that every transaction remains balanced.

Why People Are Confused About Their Use(debits vs credits)?

| Aspect | Debits | Credits | Similarity |

| Meaning | Left-side entry | Right-side entry | Both record transactions |

| Function | Increase assets | Increase liabilities | Both maintain balance |

| Usage | Expenses, assets | Revenue, equity | Used in double-entry |

| Confusion | Seen as “loss” | Seen as “gain” | Both depend on account type |

People often assume debit means “bad” and credit means “good,” which is incorrect. Their meaning depends on context.

Which Is Better in What Situation?

Debits are better when tracking expenses, purchases, and asset growth. For example, when a business buys equipment or pays rent, debits help record these increases clearly. They are essential for understanding where money is being spent.

Credits are better when tracking income, liabilities, and ownership. When a company earns revenue or takes a loan, credits provide a clear record of financial inflow or obligation. Both are equally important, and neither is better overall—they serve different purposes.

Use in Metaphors and Similes

- “Life is like a ledger; every action has its debit and credit.”

- “Her kindness was a credit to her character.”

- “His mistakes were debits in his reputation.”

Connotative Meaning of Both

- Debits: Neutral, sometimes negative (linked with expenses or losses)

- Example: “The project had many debits in terms of cost.”

- Credits: Positive (associated with gains or achievements)

- Example: “Winning the award was a credit to her hard work.”

Idioms or Proverbs Related to the Words

- “Give credit where credit is due.”

- Example: Always appreciate others’ efforts.

- “On the debit side of life.”

- Example: He focused too much on his failures.

Works in Literature

- Accounting Principles – Ray Garrison (Textbook, 2012)

- Financial Accounting – Jerry Weygandt (Educational, 2019)

- The Wealth of Nations – Adam Smith (Economics, 1776)

Movie Names Related to Both

- The Accountant (2016, USA)

- Margin Call (2011, USA)

- The Big Short (2015, USA)

Frequently Asked Questions

1. What is the basic difference in debits vs credits?

Debits increase assets and expenses, while credits increase liabilities and revenue.

2. Are debits always bad?

No, debits are not bad—they simply represent one side of a transaction.

3. Why must debits equal credits?

To maintain balance in the accounting equation.

4. Can a transaction have only debit?

No, every transaction must have both debit and credit.

5. Which is more important?

Both are equally important in accounting.

How Both Are Useful for Surroundings

Debits and credits help maintain financial discipline in businesses and households. They ensure transparency, proper budgeting, and accurate reporting. Governments and organizations rely on these principles to manage economies and resources effectively.

Final Words for the Both

Debits and credits are not just accounting terms they are the language of finance. Understanding their roles helps you manage money wisely and make informed decisions.

Conclusion

The difference between debits and credits is fundamental to understanding accounting. From simple daily transactions to complex financial systems, these concepts ensure accuracy and balance. Whether you are a beginner or an expert, mastering debits vs credits improves financial awareness and decision-making. By learning how they work together, you gain control over financial records and build a strong foundation for success.

Sarfraz Ahmad is language researcher and content writer who specializes in explaining the difference between commonly confused English words. Through WordClearify, learners understand subtle word distinctions in a simple, structured, and practical way. My writing focuses on clarity, real-life examples, and easy comparisons for students, bloggers, and professionals worldwide.